B.1 Preferred collection practices and comparison of data sources for manufacturing services on physical inputs owned by others and maintenance and repair services n.i.e.

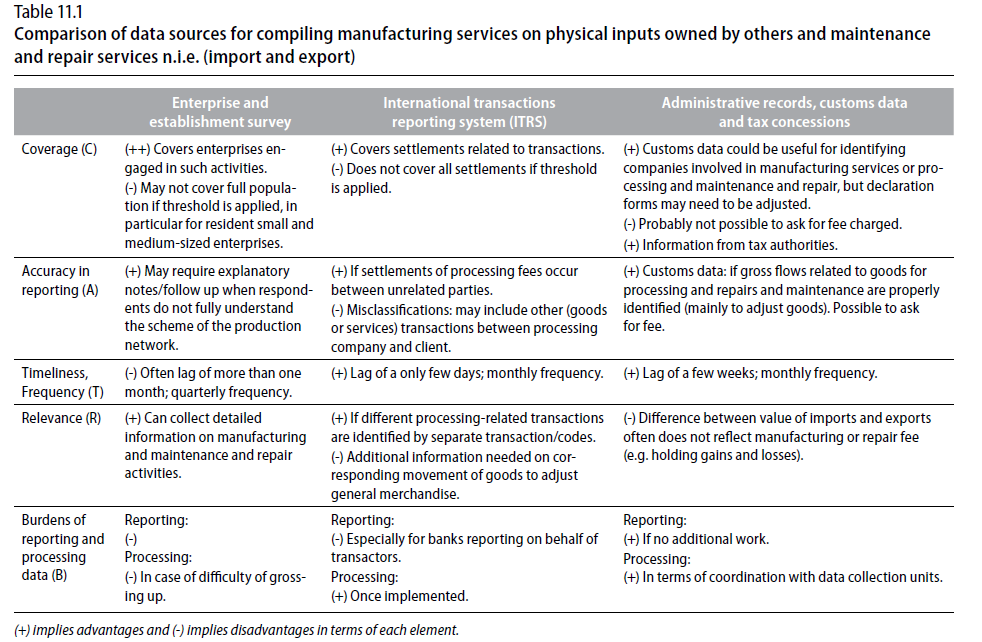

11.1. The present Guide suggests that data on manufacturing services on physical inputs owned by others (and corresponding goods) and on short manufacturing services could best be collected through surveys sent to manufacturing companies that organize international production (for imports of manufacturing services) and to processing companies/sole-proprietorships (for exports of manufacturing services). It is important to explain to respondents, and to verify that they understand, the scheme of production networks in which they are involved. Surveys would also be an efficient source for collecting information on maintenance and repairs n.i.e., paying special attention to identify separately maintenance and repairs related to construction and computer services, given the definition of those items.

11.2. An ITRS is an alternative data source for those items. For manufacturing services, it should be noted that an ITRS captures only fees paid to processors, meaning that transactions without settlements (e.g. between affiliated enterprises) may not be captured. Although customs data may also be used to derive estimates on manufacturing services, it is widely recognized that the difference between the value of imports and exports of processed goods in general does not represent the processing fee. Customs data could be useful for identifying companies engaged in processing, for reconciliation exercises when processing fees are obtained from ad hoc surveys or to complement other methods or, alternatively, as input in a data model by major type of manufacturing. Regular benchmark surveys may complement those sources to validate the model outcomes. Customs data are also potentially useful for identifying goods sent abroad for repairs and maintenance, although information on fees that is difficult to obtain could be requested in customs forms (see BPM6). Given the tax concessions provided to some firms that may be involved in processing, statements to tax authorities may provide relevant information.

Next: B.2 Good collection practices and comparison of data sources for transport